The Hall of Mirrors - Expanded and Current | Part I

Key Takeaways

- Benchmarks are shifting from descriptive to adaptive. Indices like the S&P 500 traditionally recorded market reality; now they’re changing methodology (e.g., faster inclusion of newly public mega-cap companies) to keep pace with structural shifts in how capital is raised.

- Companies are staying private longer. The rise of venture capital, private equity, sovereign wealth funds, and secondary markets means businesses can raise billions and mature for over a decade before an IPO — compared to 4-5 years historically.

- The IPO’s role has changed. Rather than financing a company’s next growth phase, IPOs increasingly just change ownership. Public investors now often buy in after the biggest growth chapters are already written.

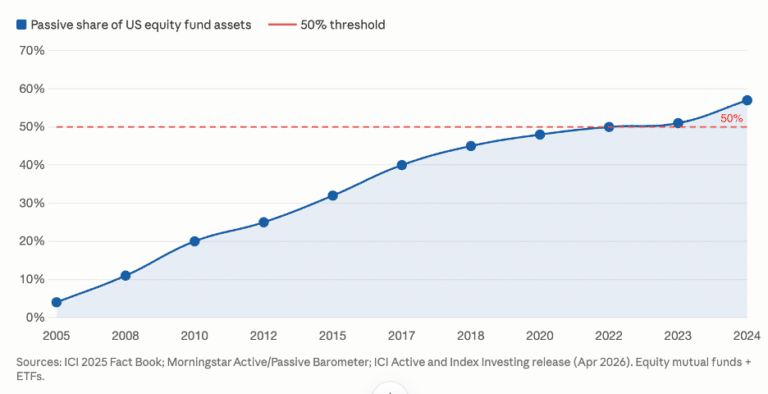

- Passive investing (Bogle’s thesis) assumed benchmarks were neutral maps. That assumption is now being tested as benchmarks actively adjust their rules to remain “representative,” raising the question of whether they still just describe the market or are starting to shape it.

- When a measurement system gains enough influence, behavior adapts to the measurement itself — a pattern seen in university rankings, hospital quality scores, and credit ratings, and now potentially emerging in market indices.

- The core question the piece poses: What happens when investors, companies, and capital start optimizing for benchmark inclusion rather than the benchmark simply reflecting the market?

There is something comforting about a good map.

A map makes no argument. It has no opinion about where you should live, which road deserves more traffic, or whether one destination is more worthwhile than another. Its responsibility is much simpler. It observes. It records. It helps us understand the landscape beneath our feet.

For much of modern investing, benchmarks served the same purpose.

The S&P 500, the Russell 1000, and countless other indices became maps of the public markets. Investors could look at them and feel reasonably confident they were seeing an accurate representation of corporate America. Companies grew. Markets assigned value. Benchmarks recorded the results. That elegant relationship helped produce one of the most important financial innovations of the last century.

Jack Bogle understood something many brilliant investors overlooked. Most people did not need a better crystal ball. They needed a better way to participate. His insight was almost disarmingly humble. Rather than trying to predict which companies would outperform, investors could simply own the market itself. Costs would fall. Taxes would become less burdensome. Human emotion would have fewer opportunities to interrupt long-term compounding. It remains one of the most successful ideas in financial history because it asked less of investors rather than more.

That philosophy depended upon a quiet assumption. The benchmark was describing the market rather than shaping it.

For decades, that assumption held remarkably well.

The public markets were where ambitious companies came to grow. A founder might raise money from family and friends, attract venture capital, and eventually seek additional financing through an initial public offering. Becoming public was less an ending than a beginning. The public markets supplied the capital needed for the next chapter of expansion, and ordinary investors participated in much of that journey.

That sequence has changed more than many investors realize.

Over the past two decades, an extraordinary amount of capital has accumulated outside the public markets. Venture capital funds have grown larger. Private equity firms manage trillions of dollars. Sovereign wealth funds search the globe for long-duration investments. Family offices increasingly invest directly in private businesses. Entire ecosystems have emerged to buy and sell shares of companies that remain privately held. Employees no longer need to wait for an IPO to create liquidity. Early investors no longer rely exclusively on public markets to realize gains. Companies that once would have listed after four or five years can now remain private for well over a decade while continuing to raise billions of dollars.

The implications reach far beyond Silicon Valley.

For centuries, stock exchanges existed primarily to connect companies that needed capital with investors willing to provide it. Railroads, steel manufacturers, telephone companies, airlines, pharmaceutical firms, software companies, and internet pioneers all relied upon public markets to finance their growth. The IPO represented an invitation to participate in the future.

Today, the future often arrives before the invitation.

By the time many of the world’s most valuable businesses become publicly traded, they have already expanded across continents, hired thousands of employees, developed mature products, and achieved valuations once reserved for entire industries. Their earliest years of explosive growth belong largely to private investors. The public offering increasingly serves a different purpose. It changes shareholders more often than it finances innovation.

That distinction deserves more attention than it has received.

Consider the experience of an ordinary investor. Twenty-five years ago, purchasing shares shortly after a company’s initial public offering often meant joining the story while many important chapters remained unwritten. Today, purchasing shares after a major IPO may mean arriving after years of private funding rounds, secondary transactions, employee tender offers, and institutional ownership. The company may still possess remarkable opportunities ahead. Yet the journey between founding and public ownership has become dramatically longer.

This is not a criticism of private capital. Quite the opposite. Private markets have financed extraordinary innovation and allowed businesses to pursue ambitious ideas without the relentless pressure of quarterly earnings expectations. Many of history’s most important technologies may never have reached maturity under the older model. Every evolution in capital formation solves real problems.

Every solution, however, introduces new incentives.

Those incentives rarely announce themselves. They emerge gradually as intelligent people adapt to changing conditions. Companies remain private because capital is available. Investors create secondary markets because liquidity has value. Institutions allocate more money to private assets because opportunity appears attractive. None of these decisions requires coordination. Each one makes sense on its own. Together they reshape the landscape.

Eventually, the maps must change as well.

Imagine attempting to build a benchmark of the American economy while excluding one of its largest and most influential companies simply because it recently became public. The benchmark would become less representative of the market it claims to describe. Index providers have recognized this challenge. As initial public offerings become larger and companies arrive in public markets at unprecedented scale, benchmark methodologies have begun adapting. Waiting a year or more before adding a trillion-dollar company may faithfully follow yesterday’s rules while poorly describing today’s market.

That adaptation is understandable.

It is also historically significant.

For the first time in a meaningful way, the benchmark is adjusting itself to accommodate structural changes in how capital is formed, how companies mature, and how ownership evolves. The map is changing because the landscape has changed.

Most investors stop their analysis there.

The more interesting question begins there.

What happens when a map becomes important enough that people start building roads because of it?

That question extends well beyond investing. Universities respond to rankings. Hospitals respond to quality scores. Companies respond to credit ratings. Search engines shape what we read by determining what we see first. Every measurement system eventually acquires influence over the thing it was originally created to observe.

Markets may be approaching a similar moment.

The benchmark still describes reality. It may also be beginning to shape it.

That possibility deserves thoughtful examination, because understanding markets has never been only about studying companies. It has always required studying incentives. Capital flows toward opportunity. Rules influence capital. Architecture influences behavior. The most important changes in investing often begin quietly, long before they appear in performance reports.

The next question is where those incentives lead.

That is where our story continues. Part two coming soon.

Lauren Pearson is the founding partner and Managing Director of Somerset Advisory, an independent wealth management firm built to serve the complex needs of multigenerational families, entrepreneurs, and executives.

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson

- Lauren Pearson